Why Your Credit Score Dropped and How to Raise It

Find out how your credit score can drop, plus 13 tips for managing credit

Unlocking the mystery behind a sudden drop in credit score can be a financial game-changer. Fortunately, pulling your credit reports is a quick, straightforward way to investigate the reasons behind your credit score changes. Plus, you'll gain insights on how to fix your score. A healthy credit profile is your ticket to financial freedom - so it's time to dive in and learn how to make your credit work for you.

How can you find out why your credit score dropped?

Finding out why your credit score dropped involves obtaining a copy of your credit report and examining it for any negative changes. Here's a step-by-step guide on how to do this:

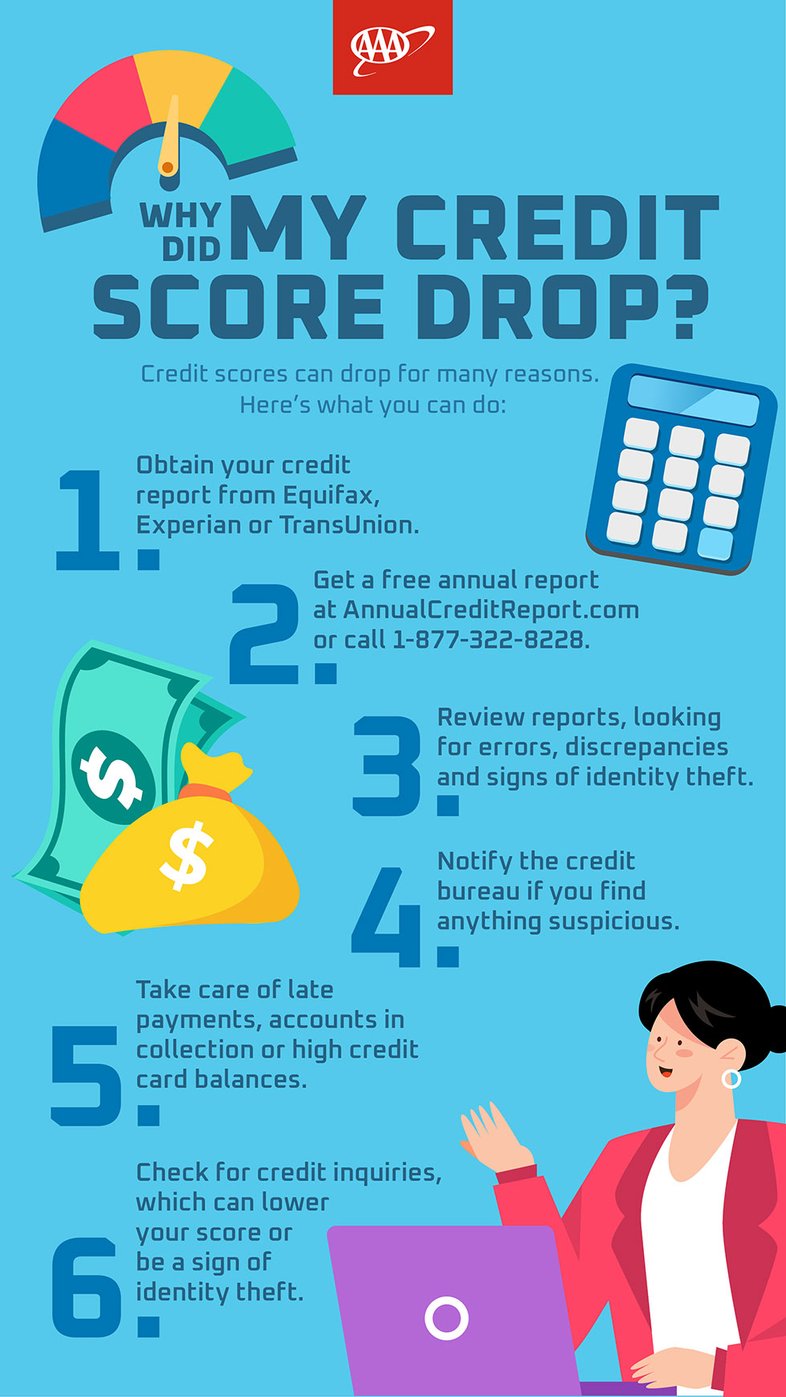

Obtain your credit reports from the three major credit bureaus (Equifax, Experian, and TransUnion). You can get them online, by phone, or by mail. For your free annual credit report you can visit AnnualCreditReport.com, call 1-877-322-8228, or mail the request form to Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281.

Review the reports carefully. Look out for anything fishy— discrepancies, errors, or unfamiliar accounts. If you spot any, don't hesitate—give the credit bureau a heads-up. Also, look for signs of identity theft. If you suspect fraudulent activity, visit identitytheft.gov for assistance.

Search for factors that could negatively impact your credit. Be on the lookout for late payments, accounts in collections, or high credit card balances. If you do spot one of these issues, no need to stress. Take charge and address them directly by ensuring your bills are paid on time and steadily reducing your debt.

Check for recent credit inquiries. Too many in a short time can give your score a beating. If you didn't initiate certain inquiries, it could signal potential identity theft.

Consider utilizing credit monitoring services. These services offer real-time updates on your credit reports, allowing you to stay informed about any changes or suspicious activities that may affect your creditworthiness.

Reasons why your credit score can drop

It’s crucial to understand the reasons your credit score can drop so you know what to check for on your credit report. Some of the reasons are due to your borrowing behavior, while others can occur even when you’re doing an excellent job managing credit.

Payment history heavily influences your credit score. Any late or missed payments on loans, credit cards, or other debts will have a negative impact.

Accounts in collections or legal judgments result in derogatory marks, causing your credit score to drop.

Bankruptcies and foreclosures are major financial events that severely damage your credit.

Every new credit application triggers a hard inquiry on your credit report, which lowers your score. Multiple inquiries worsen this effect.

Taking out new loans increases your credit utilization ratio, as does closing a credit card account since it reduces your borrowing capacity.

While paying off a loan is generally positive, it can temporarily lower your credit score due to a reduction in your credit mix. A diverse debt portfolio can boost your score.

Inaccurate information, such as erroneous accounts or payment statuses, can negatively impact your credit score. • Identity Theft: Unauthorized accounts and transactions resulting from identity theft can wreak havoc on your credit.

Tips for increasing your credit score

Building good credit takes time, but you can make strides toward a higher score through consistent effort and responsible financial habits. Here's how to increase your credit:

Staying on top of your bills is key. Whether it's credit cards, loans, or any other accounts, timely payments build a solid borrowing history that boosts your credit.

Keeping your credit card balances below 30% of your credit limit is the sweet spot for maintaining a healthy credit utilization ratio.

Opening too many credit accounts in a short span can raise eyebrows. Instead, be strategic about opening new accounts to avoid multiple hard inquiries, which can hint at risky borrowing behavior.

Make it a habit to review your credit reports annually for any hiccups. If you spot errors or inconsistencies, don't hesitate to dispute them to ensure your credit info is spot-on.

Diversifying your credit portfolio—think credit cards, installment loans, and mortgages—can give your credit score a nice little boost.

Your long-standing credit accounts are like gold. The longer your credit history, the better your score tends to be, so think twice before closing those old accounts.

If you're in a tight spot, don't be afraid to reach out to your creditors. They might be willing to work with you on payment plans or settlements to help you manage your debts more effectively.

Focus your efforts on paying off those lingering debts, especially those high-interest credit cards and any accounts in collections.

Be mindful of how you wield your credit. Responsible use—like making timely payments and keeping credit utilization in check—is the name of the game for a positive credit profile.

Setting up a budget is a game-changer for managing your finances and steering clear of overspending.

Avoid those pesky late payments by setting up handy reminders. Many banks offer automatic payments or reminders to keep you on the ball.

If there are any negative marks on your credit report, tackle them head-on. Whether it's setting up payment plans or negotiating settlements, taking action can help improve your credit standing.

Remember, improving your credit score is a marathon, not a sprint. Stay patient and persistent as you practice good financial habits over time.